This paper investigates whether the returns of stocks that are connected through mutual fund owners covary more together. In addition, the paper explores the implications of such comovement arising from common institutional ownership in predicting return variations, from which an implementable trading strategy is devised. A natural experiment for establishing causality is introduced, and how hedge funds may contribute to the occurrence of the documented phenomena (results) is also discussed.

The paper has an intellectual link to contagion, which can be defined as excess correlation, or, correlation over and above what one would expect from economic fundamentals. It is also related to the literature on fund flows and institutional-driven price (co)movements, which provides the ground for the assertion that the presence of institutional connectedness may generate cross-stock reversal patterns in returns, especially when the price pressure from fund flows reflects forced selling.

[Data, Sample, and Measurement of Common Ownership]

Common stocks whose market caps are above NYSE median market cap (i.e., big stocks) are retained in the sample. This ensures that the documented patterns are not just due to small or microcap stock effects. Also, common ownership by active managers is not pervasive, especially among the small stocks. The sample period spans from 1980 to 2008.

Common ownership is measured at each quarter-end as the total value of stock held by F common funds of the two stocks, scaled by the total market capitalization of the two stocks. It can be formalized as below;

where f is related to the funds that own shares for the firm pairs (i, j). S denotes the number of shares, and P denotes price at a certain time period.

[Regression Model]

After constructing the common ownership measure as well as other relevant control variables, the following regression model is estimated for predicting cross-sectional variation in comovement;

where the dependent variable represents the within-month realized correlation of each stock pair's daily four-factor residuals in month t+1. Rather than the pooled OLS, Fama-MacBeth regression with Newey-West standard error is used to address any cross-correlation issues in the residuals as well as autocorrelation in the time series.

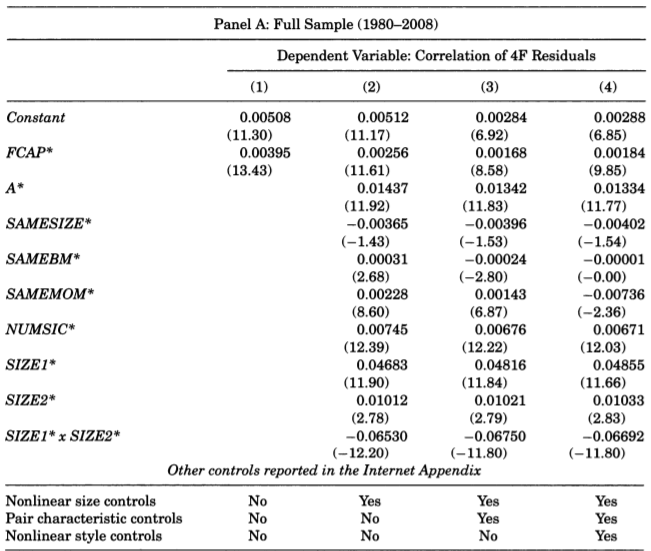

[Results]

The table below presents the results from estimating the regression model described above;

Across different specifications, we can see that the coefficients for FCAP are positive and statistically significant, meaning that the degree of connectedness among a pair of stocks via common institutional ownership strongly positively predicts cross-sectional abnormal return correlation as measured by four-factor residual correlations.

[Endogeneity Concern and Natural Experiment]

The results presented above are subject to the endogeneity concern that fund managers may choose to hold similar stocks. To establish causality, the paper exploits a natural experiment based on the mutual fund scandal that occurred in September 2003. Because the implicated families during the scandal experienced significant outflows, it can be argued that the suggested scandal provides an exogenous shock to capital flow, helping to eliminate concerns that the results are driven by the endogenous choices by fund managers. The instrument adopted here is RATIO, which is the total value held by all common 'implicated' funds of the two stocks over the total value held by all common funds. Two-stage least squares regression (2SLS) is estimated. The results are shown below;

Again, across all specifications, the coefficients for the instrumented FCAP are statistically significant, allowing causal interpretation of the results. Also, the fact that most coefficients are insignificant under simple OLS estimation reflects that the endogeneity of common ownership may genuinely be an important issue.

[Cross-Stock-Reversal Strategy]

A profitable trading strategy given the results documented above is to buy (sell) stocks that have gone down (up) if their connected stocks have gone down (up) as well. The underlying intuition is, if we have a highly-connected pair of stocks (i, j), if stock i experiences a negative shock and connected stock j's price also drops, one may conjecture that i's drop is due to price pressure related to fund trading but less to fundamentals, which we expect to revert. In other words, the trading strategy exploits the temporary misvaluation that may arise from mutual fund trading, with the degree of connectedness used as a measure of the extent of that temporary misvaluation.

The figure below presents the cumulative alphas over time for such a trading strategy;

We can clearly see that the long-short portfolio generates positive cumulative alpha. Also, more of the effect comes from the low portfolio than the high portfolio, consistent with the forced selling/price pressure story.

[Hedge Fund]

Lastly, the paper explores whether the activities by hedge funds either benefit from or exacerbate the documented contagion generated from ownership-based connections.

The table below shows hudge funds' exposure to the strategy exploiting the institutional connectedness (CS strategy);

As the results indicate, hedge funds, especially those that exploit long-short strategy, negatively load on the CS factor and more so when the change in VIX is high. It appears hedge funds do not take full advantage of the opportunities that price pressure from mutual fund flows provide, exacerbating rather than mitigating the comovement patterns documented throughout the paper.

No comments:

Post a Comment