In this paper, Shiller analyzes the efficient market model based on the idea that stock prices are the present value of their future dividends. He finds that the volatility of dividends is too small to account for the volatility stocks. The author explores this model of efficient markets and derives inequalities to bound the standard deviations of changes in price and price innovations. He also analyzes implications for the time variance of the real discount rate on prices.

To demonstrate the motivation behind his analysis, Shiller presents the real S&P index (p) and the associated ex post rational dividend price (p*) in Figure 1 along with that of the Dow Jones Industrial Average in Figure 2. The large variation in the index compared to that of the dividend forecast is clearly seen. Although there is variation in dividends over the period none of it is substantial enough to cause a large change in p* since the p* series represents a moving average of dividends with the discount factor as the weight.

Events such as the great depression are seen in the chart where a steep decline in stock prices occurs but without a large associated change in future dividends. Could such large stock movements be rationalized by mistaken forecasting errors regarding future dividends? Shiller compares stock and dividend volatility to argue that this is not the case.

In a rational market, the price of stocks should reflect the best estimates that can be made with all available information. Mathematically, $p_t=E_t(p_t^*)$ indicates that the price at time t is the expectation, conditional on the available information at time t, of p*. Assuming the forecast error is uncorrelated with prices, Shiller derives an inequality for the standard deviation:

\[(1) \hspace{120pt} \sigma(p) \leq \sigma(p^*)\]

I.e. the standard deviation of rational prices must be less than or equal to the deviation of the predicted prices given available information. This is clearly violated by Figure 1.

Equation (2) gives the basic efficient markets model that will provide the basis for the paper’s analysis. The price at time t is the sum of the expectations of future dividends conditional on information at time t, scaled by the constant real discount rate $\gamma$.

\[(2) \hspace{120pt} P_t = \sum_{k=0}^{\infty} \gamma^{k+1} E_t D_{t+k}\]

This model can be rewritten in terms of price innovations, $\delta_t p_t \equiv E_t p_t + E_{t-1} p_t$. Equation (5) represents innovations in price in terms of innovations in dividends.

\[(5) \hspace{120pt} \delta_t p_t = \sum_{k=0}^{\infty} \gamma^{-k+1} \delta_t d_{t+k}\]

Shiller shows that if the variance of price innovations is to be maximized, the dividend innovations must be related to its lag by a moving average, giving it an autoregressive integrated moving average form. Performing the maximization gives an inequality for the standard deviation of price innovations in terms of the deviation of dividends and the two period interest rate, $\bar{r_2}$. Note that $\delta_t p_t \equiv \Delta p_t + d_{t-1} - \bar{r} p_{t-1}$.

\[(11)\hspace{120pt} \sigma (\delta p) \leq \frac{\sigma (d)}{\sqrt{\bar{r_2}}}\]

This can also be formulated to express the standard deviation in price change, $\Delta p$, with respect to the standard deviation of dividends, where $\Delta p_t = \delta_t p_t + \bar{r} p_{t-1} - d_{t-1}$.

\[(13) \hspace{120pt} \Delta p \leq \frac{\sigma (d)}{\sqrt{2 \bar{r}}}\]

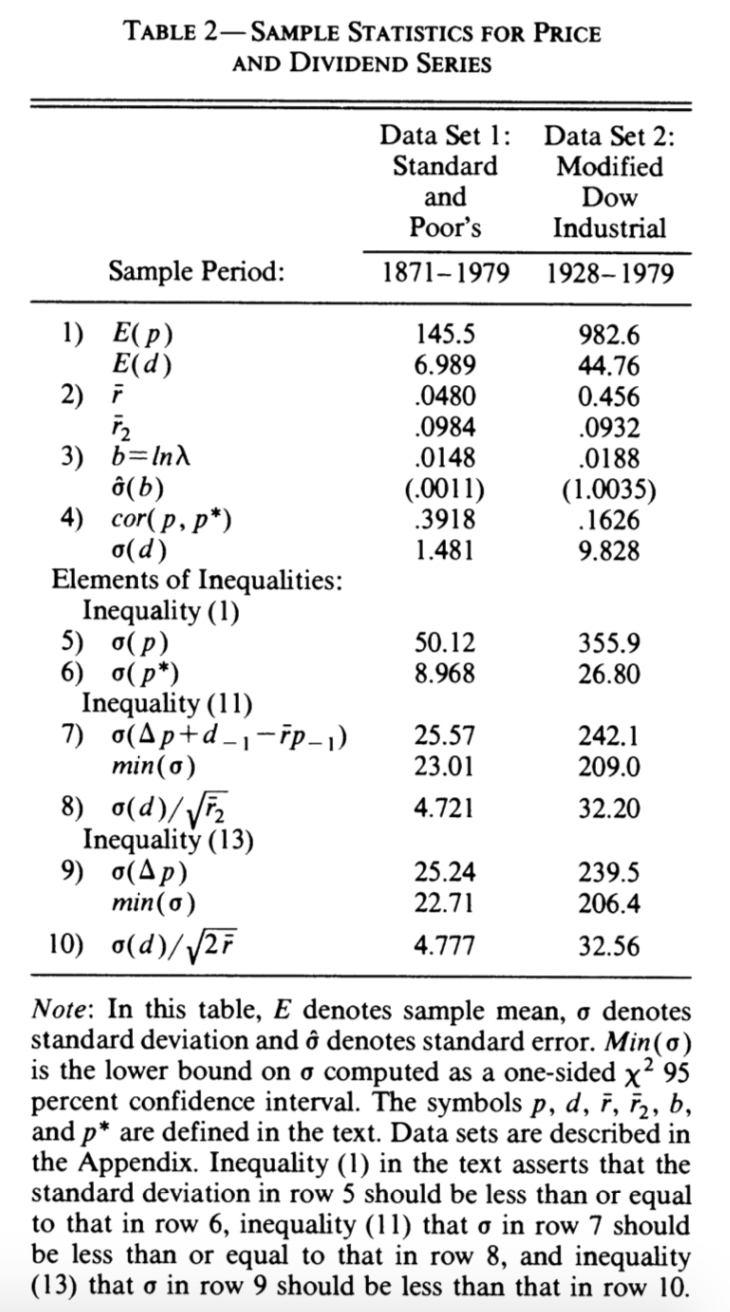

Equations (11) and (13) provide the bases for the empirical tests used in this paper, the results of which are reported in Table 2. Lines 1-4 provide the estimated values for the terms used in the calculations. The subsequent lines present the values for both sides of inequalities (1), (11), and (13). All three inequalities are violated, with the left hand side at least five times, and up to thirteen times, greater than the right hand side.

The model so far has assumed a fixed real discount rate, $\bar{r}$. If the real discount rate was allowed to vary across time, perhaps it could account for the difference in the left and right hand sides observed in Table 2. Shiller derives equation (17) to find a lower bound for the standard deviation of the expected real interest rate.

\[(17) \hspace{70pt} \sigma (\bar{r}) \geq \big(\sqrt{2E(\bar{r})} \:\sigma (\Delta p) - \sigma (d)\big) E(\bar{r}) / E(d)\]

Using this he finds that the real interest rate, $\bar{r_t}$, would need to have a ±2 standard deviation range of -3.91 to 13.52 percent for data set 1 and -8.16 to 17.27 for data set 2 to explain the discrepancy between line (9) and (10) in Table 2. Shiller claims that this is the lowest possible variability in the real interest rate that is possible if the observed volatility in dividends is to explain the accompanying volatility in stock prices.

This paper evaluates a model of market efficiency that states stock price in terms of the discounted value of future dividends. Under this model, changes in stock price are explained by new information regarding future dividends. By empirically measuring the standard deviation of real dividends and assuming this represents the uncertainty of information on future real dividends, Shiller shows that the volatility of stocks is five to thirteen times too high to be explained by the deviation in dividend information. Even if the real discount rate is allowed to vary across time it would have to be very large to account for the variation in stock prices. Although Shiller does not claim to disprove the theory of market efficiency, he shows that in this particular model, the discounted price of dividends cannot fully explain the variation in stock prices.

No comments:

Post a Comment